“What is GTL on paystub?”

GTL means Group Term Life insurance, which is a benefit given to employees by companies. Employees don’t have to pay this premium proportionally as it is fully paid by employers.

The first $50,000 is a tax-free amount, while more than this is considered imputed income. This is how GTL on your paycheck increases your taxable income even when you don’t get anything in your pocket.

Quick Answer

GTL on paystub is known as Group Term Life insurance. Many companies offer this benefit to their employees. The very first coverage of $50,000 is completely tax-free, while amounts above are considered imputed income by the IRS (Internal Revenue Service). It is added to your taxable income; however, the premium does not come from your salary.

What is GTL on Paystub?

GTL full form in insurance is Group Term Life Insurance, which is a single, company-paid life insurance benefit covering a large group of employees.

When you notice GTL on a paystub, it is the amount of the company-paid life insurance benefit. The benefit of GTL is that it does not cost you anything. It gives a fixed amount to your designated beneficiary in case you pass away during the coverage period. This insurance ends when you leave the job.

Facts you must know about GTL on your paystub:

- Your company pays for your life insurance coverage.

- Up to $50,000 coverage is completely tax-free.

- Coverage exceeding $50,000 adds to your taxable wages.

Note: Group Term Life is a common type of coverage that doesn’t affect your take-home salary directly, but it increases your taxable income.

Here is the breakdown of the GTL word by word:

| Word | What It Means |

| Group | A common policy that covers a number of employees |

| Term | Means a set of periods until you leave the job |

| Life | Pay for life coverage if you pass away during the coverage period. |

Tip: Some companies allow you to buy additional coverage on your basic plan. This extra coverage is paid from your own salary deductions.

This group term life insurance is completely different from a policy you buy for yourself. As the company buys a common plan for all, the cost per employee is lower. This insurance is tied to your job and ends when you leave or retire from your job.

How Group Term Life Insurance Works for Employees

GTL is a life insurance benefit that your company pays for all eligible workers. The company buys a single policy for a large number of employees rather than individual policies.

Formula to calculate GTL

Monthly imputed income = [(Total coverage − $50,000) ÷ $1,000] × Table I rate for your age

Annual imputed income = Monthly imputed income × 12 − Employee after-tax contributions

Quick Facts About GTL Insurance:

- Who pays GTL insurance?

The company pays, but the premium plan over the basic plan comes from the employee’s income.

- Is GTL mandatory for all companies?

No, it is up to your company’s benefit plans.

- Are all employees eligible for it?

The company decides on eligibility criteria and plan rules.

- Is GTL coverage taxable?

More than $50,000 is taxable.

- Does GTL reduce take-home pay?

It doesn’t reduce your take-home salary directly but increases the taxable amount.

Example of how GTL coverage works for taxable income.

| $25,000 | Tax-free GTL income |

| $50,000 | Tax-free GTL income |

| $800,000 | The extra $30,000 is GTL imputed income. |

If you understand how GTL insurance works, you know everything on your paystub and can clear up confusion while filing taxes.

Note: For claiming GTL insurance, nominees should inform the company or insurer and submit all the necessary documents, such as the claim form, death certificate, and proof of identity.

What Is GTL Imputed Income?

GTL imputed income is the taxable amount of a company-paid life insurance policy for more than $50,000. The IRS considers this additional coverage a real value benefit, so the GTL imputed amount is the value with the dollars added to your taxable net income, even when you don’t get anything on your pay stub.

Important things to know about GTL imputed income;

- It is a non-cash benefit that you get.

- It adds to your total taxable net income.

- The first $50,000 is tax-free, which means you have to pay tax on the amount exceeding that.

- The Internal Revenue Service set a standard table value.

Important: GTL imputed income comes under Social Security and Medicare taxes. The federal income tax withholding may be different on it; therefore, it is better to check with your HR or payroll team for more details.

To understand the GTL imputed meaning in a simpler way is to consider it as a benefit that has a price tag. The Internal Revenue Service (IRS) strongly believes that company-paid insurance coverage of more than $50,000 is a big value; therefore, it takes it as additional pay.

Although you don’t get this amount in your account, you must pay tax on it. It decreases your net income even when you did not pay any premium for the insurance.

Note: Companies decide the eligibility criteria for GLT. Full-time workers are normally covered for GTL. Some companies extend this insurance to contract employees and new joiners, covering a waiting period. However, age limits, coverage, and benefits can be different depending on the company and insurer.

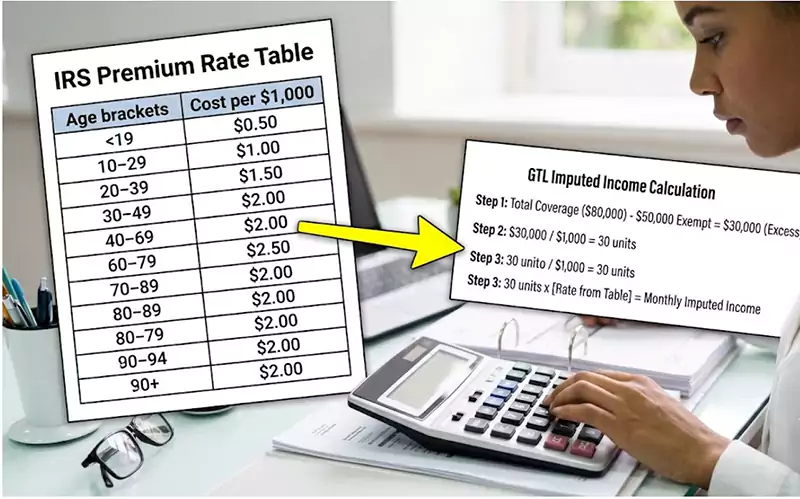

How is GTL Imputed Income Calculated?

We calculate the GTL imputed income with the help of an IRS standard table, depending on your coverage amount and age. The IRS increases the cost by $1,000 for coverage exceeding $50,000. The company multiplies the rate by your extra coverage to get the exact GTL imputed income added to your net pay for each taxable year.

Here are the basic calculation steps:

- Subtract $50,000 from the net coverage.

- Divide the remaining by 1,000 to have exact units.

- Match your rate as per age from the IRS standard table.

- Multiply these units by the monthly rate from the table.

- Subtract the amount of premiums if you pay any amount yourself.

Example: Suppose your coverage is $80,000, and only $30,000 is the taxable amount in it. That is only 30 units after dividing it by $1000. Multiply the IRS rate according to your age; this is how you can calculate the actual monthly imputed income.

The monthly rate increases as you become older because the IRS table is completely based on age. It means a younger employee pays a lower amount for every $1,000 in comparison to an older employee. This is the reason why 2 employees with the same coverage amount get different GTL imputed income values on their pay stubs.

There is a simple version of the Code of Federal Regulations standard table by age;

| 5-year age bracket | Cost per $1,000 of monthly protection |

| Under 25 | $0.05 |

| 25 to 29 | 0.06 |

| 30 to 34 | 0.08 |

| 35 to 39 | 0.09 |

| 40 to 44 | 0.1 |

| 45 to 49 | 0.15 |

| 50 to 54 | 0.23 |

| 55 to 59 | 0.43 |

| 60 to 64 | 0.66 |

| 65 to 69 | 1.27 |

| 70 and above | 2.06 |

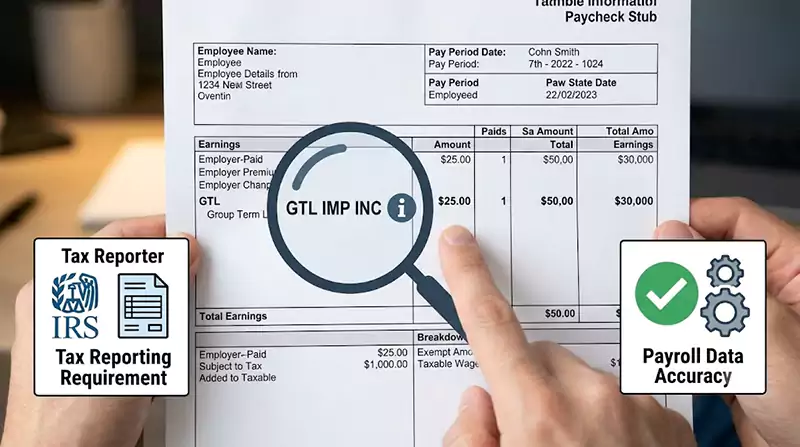

What Is GTL on Your W-2 Form?

The GTL calculated income is available on your W-2 form in box 12 with code C. During tax filing, the value of GTL on your W-2 form is already calculated in your Box 1 taxable value. Record C generally shows the actual taxable cost of group term life insurance for more than $50,000.

This is where GTL is available on your W-2 form:

| W-2 Spot | What It Shows |

| Box 1 | Total taxable wages with GTL amount |

| Box 12, Code C | Taxable amount of Group Term Life over $50,000 |

| Boxes 3 and 5 | Wages subject to Social Security and Medicare |

Note: You personally don’t need to do additional calculations while filing taxes. Your company already calculates the GTL value correctly, so it automatically goes into your return.

Why GTL Shows Up on Your Paycheck

The amount of GTL appears on your pay slip so that the taxable value of your insurance can be calculated and taxed correctly. When you see GTL on your paycheck, it means that your company reports the added income of more than $50,000. It maintains your tax and payroll records correctly for the year.

Here are some common reasons why you see GLT on your paycheck:

- Your insurance coverage is more than the limit of $50,000.

- The Internal Revenue Service needs the extra value for taxation.

- Your company considers it imputed income.

- Federal Insurance Contributions Act (FICA) taxes are applicable to the added amount.

When you ask your HR or payroll team, “What does GTL mean on a pay stub?” on your paycheck, it means that your employer does the necessary reporting. It does not mean that the amount is deductible for the insurance from your take-home salary.

You probably see that the label varies from one employer to another. Some payroll systems show it as “GTL,” while others show it as “GTL imp income” or Group Term Life.

Dos and Don’ts With GTL on Your Paystub

Dos

- Confirm the amount of your coverage with your HR

- Check your recent salary slip for the GLT line

- Make sure the beneficiary is updated carefully

- Ask the payroll team if the amount looks different

Don’ts

- Don’t think the amount of GLT is deductible from your take-home salary.

- Don’t let it out of your mind that coverage ends as soon as you resign.

- Don’t overlook GLT on your W2 when filing taxes.

Conclusion

Now you must be aware of what is GTL on paystub. GTL is Group Term Life Insurance, which your company pays for you. The very first amount of $50,000 coverage is completely tax-free.

However, the coverage exceeding $50,000 is taxable, which is calculated directly in your taxable income. You must understand that it is a benefit and not a deduction; therefore, it doesn’t affect your take-home salary.

Next Step: Download your most recent salary slip and check your GTL area to know your insurance amount and beneficiary details from your payroll team or HR.

FAQs

1. What does GTL mean on a paystub?

Ans: GTL stands for Group Term Life insurance, which your company pays for. It shows as the taxable value of coverage over $50,000 on your pay slip as imputed income.

2. Is GTL deducted from my paycheck?

Ans: No, the basic Group Term Life insurance is paid by the company; thus, it is not deductible from your salary. However, the taxable value of more than $50,000 is included in your pay for tax purposes.

3. What is GTL imputed income?

Ans: GTL imputed income is the taxable value of employer-paid life insurance above $50,000. The IRS treats it as income, so it is added to your wages and is subject to Social Security and Medicare taxes.

4. Where does GTL show on my W-2?

Ans: Group term life insurance is available in Box 12 with code C on your W2. Don’t worry, this amount already consists of your Box 1 taxable amount; thus, you do not need additional calculations during tax filing.

5. Is the first $50,000 of GTL taxable?

Ans: No, the very first amount of $50,000 of GTL coverage is completely tax-free under the Internal Revenue Service (IRS). The value of more than $50,000 is considered taxable imputed income.

- Group-term life insurance by the IRS

- General Instructions for Forms W-2 and W-3 (2026) by the IRS

- Code of Federal Regulations by ECFR

{kind=link}